.webp)

Help our experts understand you better by filling our 2-Minute Form, to find the right education loan

Get instant loan offer suitable to your profile !

On this Page:

Most students think SBI sanction means money is ready. It doesn't. Here's where documentation actually fails in the disbursement process — and why RACPC delays matter more than your branch.

Quick Summary:

The SBI education loan disbursement process is where most students discover that loan approval and money in hand are two very different things. Your sanction letter confirms the bank trusts you. But disbursement is where the bank verifies every rupee you're asking for and this is where documentation errors, unclear expense breakdowns, and processing bottlenecks cause the most damage.

As per data shared by the Ministry of Finance in the Rajya Sabha and reported by The Indian Express, State Bank of India has disbursed over ₹32,311 crore in education loans over a recent three-year period, making it the largest lender in this segment among public sector banks. This scale also means high volume processing, which directly impacts how long individual disbursement requests take to clear, especially during peak admission cycles between May and August.

For students, the risk is simple: delays in the SBI loan disbursement process can derail visa timelines, jeopardize seat confirmations, and force last-minute scrambles for alternative funding. Many assume the hard part is over once the sanction letter arrives. In reality, the education loan disbursement SBI stage is where preparation, clarity, and follow-up matter most.

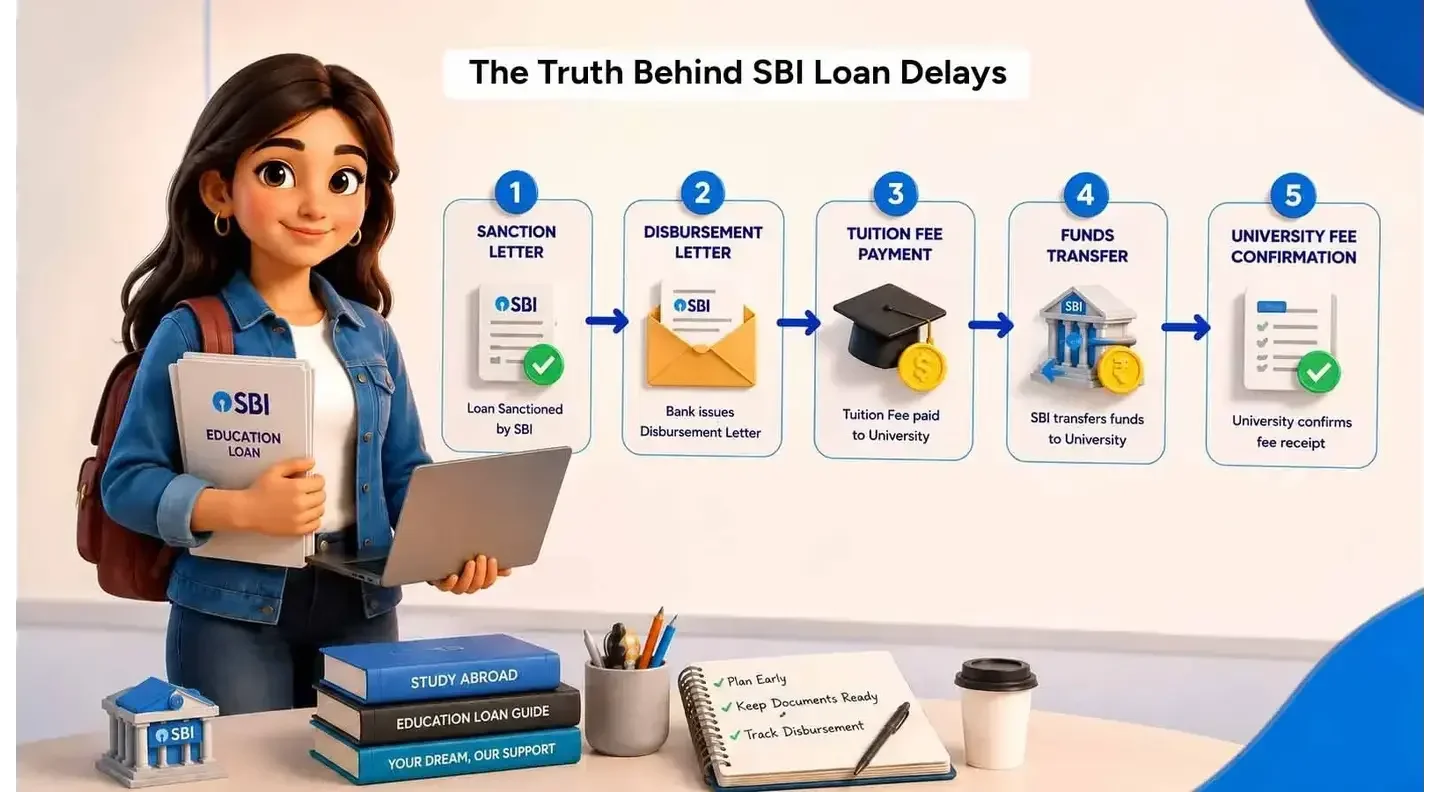

In the SBI education loan disbursement process, sanction and disbursement serve completely different functions, yet students treat them as the same milestone. This misunderstanding is the root cause of most disbursement delays.

Sanction Letter:

Disbursement Letter:

The gap between these two stages is where most students lose time. They assume sanction means money is ready to move. In reality, disbursement depends entirely on how clearly you can justify each expense you're requesting.

Why This Matters: Universities and visa authorities operate on fixed deadlines. If you submit your disbursement request with incomplete documentation, say, a vague "living expenses estimate" instead of a detailed rent agreement and monthly cost breakup, SBI's RACPC will hold the request until you provide clarity. By the time you correct it, your fee deadline may have passed.

Most students believe their local SBI branch controls disbursement timelines. This is incorrect.

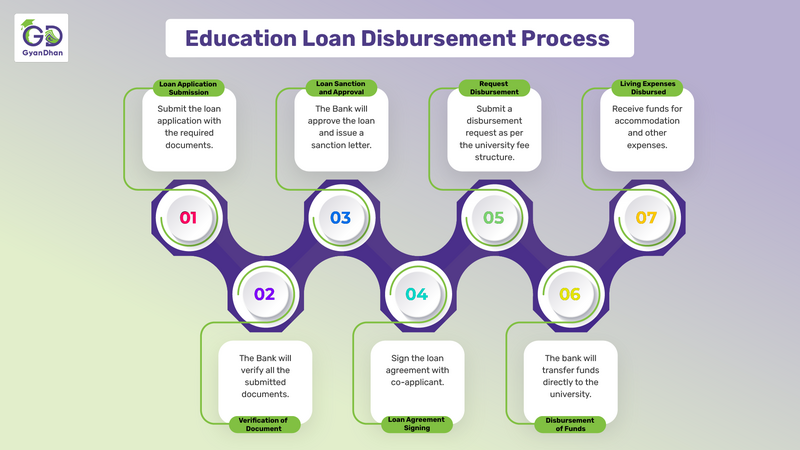

Once your sanction is approved and you submit disbursement documents, your file moves to SBI's Retail Assets Central Processing Cell (RACPC). This centralized unit handles bulk verification and fund release for all education loans across regions. Your branch uploads your documents, but RACPC reviews them, cross-checks university payment instructions, validates expense proofs, and executes the transfer.

What this means in practice:

The Pattern: Students who proactively coordinate between their branch and RACPC, verify document formats before submission, and provide complete expense breakups in the first attempt typically experience faster disbursement. Those who assume "the bank will figure it out" end up in multi-week loops.

To understand where documentation actually fails in the education loan disbursement SBI, here's a real-world case shared by GyanDhan's education loan counselors:

Riya, heading to the University of Toronto for her MS, received a ₹40 lakh sanction from SBI. She assumed the next step was straightforward: submit her fee demand letter and wait for the money. What slowed her down wasn't the bank's processing speed it was her incomplete cost breakup.

What Went Wrong:

SBI's RACPC flagged the request and sent it back to the branch for corrections. Riya had to provide:

Once corrected, SBI processed it in stages:

The Takeaway: The SBI loan disbursement process doesn't fail because of bank inefficiency. It fails because students submit expense requests without the clarity banks legally require to release funds. The more specific your documentation, the faster your disbursement moves.

Before entering the SBI education loan disbursement process, every applicant must route their loan application through the Vidya Lakshmi Portal, as mandated for all public sector banks under the National Scholarship Portal framework.

Even if you initiate your loan through a branch, SBI internally aligns your application with this system for compliance tracking. Skipping or delaying this step can slow down your overall education loan disbursement process because RACPC cross-references your file with Vidya Lakshmi records during verification.

Portal Access: Vidya Lakshmi Portal

Most students focus on sanction amount and interest rates. What they miss is how SBI's margin money requirement directly affects disbursement complexity. Here's what matters during the education loan disbursement SBI stage:

Margin Money (10% of total expenses): If your total cost is ₹20 lakh, SBI funds ₹18 lakh and you contribute ₹2 lakh. The problem? You must specify in your disbursement request which expenses are margin-funded versus loan-funded. Students who submit requests without this breakdown get flagged immediately at RACPC.

Processing Timeline (20-25 days after collateral): This is a sanction timeline, not disbursement. The actual SBI loan disbursement time after sanction is 5-10 days but only if documentation is perfect. Most students confuse these two timelines and end up missing fee deadlines.

Moratorium Period (Course + 6 months): This affects disbursement strategy for multi-year programs. Students who understand this request Year 1 expenses only, keeping Year 2 funds for later disbursement against fresh fee demands. Those who try to disburse everything upfront face unnecessary verification delays.

Interest rates, loan amounts, and other standard parameters are available on SBI's website. What actually determines your disbursement experience is how well you understand these three structural elements before submitting your first request.

A common question in the SBI education loan disbursement process is whether funds can be released before visa approval. The answer is yes — but only when required by the destination country or university as part of visa compliance.

Countries Where Pre-Visa Disbursement Is Common:

How This Works: In such cases, SBI transfers funds to the respective institution or designated blocked account before you receive your visa. This is not "early access" to loan money — it is tightly linked to visa compliance requirements.

Critical Point: Submitting the wrong payment format such as sending GIC funds to a personal account instead of the official GIC provider, or transferring blocked account funds to a non-approved German bank can delay both your visa and the education loan disbursement process. Always verify exact payment instructions from the destination country's immigration authority before requesting disbursement.

For living expenses in pre-visa scenarios, SBI may also load funds onto a forex card. These cards typically have a 3-month validity, and unused funds may require revalidation or reissuance depending on usage timelines and travel delays.

The Pre-Visa Disbursement Misconception: Many students assume pre-visa disbursement speeds up their process. It doesn't. It shifts the bottleneck from SBI to visa authorities. Once SBI transfers your GIC to Canada or blocked account funds to Germany, you're now waiting on immigration processing which SBI cannot control. Pre-visa disbursement doesn't make you faster; it makes you compliant with visa requirements that would delay you anyway. The actual time saved is zero. What changes is when you encounter the delay: before SBI disbursement or after.

Based on patterns observed across thousands of SBI education loan applications, here are the most common documentation failures that delay the education loan disbursement SBI:

Unclear University Fee Demand Letters Students submit demand letters that show total tuition but don't break down:

SBI needs granular clarity because they transfer tuition directly to the university. Vague totals get flagged.

Without this, your living expense disbursement request stalls.

These errors trigger automatic rejections at RACPC.

Vague Miscellaneous Expenses Estimates Requesting ₹3 lakh for miscellaneous expenses without itemization (health insurance, study materials, gadgets, travel) raises red flags. SBI expects:

The more specific your breakdown, the faster your request clears.

Co-Applicant KYC Expiry If your co-applicant's KYC documents (PAN, Aadhaar, income proof, tax returns) are outdated or expired by the time you request disbursement, SBI will hold the file until fresh documents are submitted. This is especially common when students delay disbursement requests for several months after sanction.

Students often ask: "Why can't SBI just release the full sanctioned amount at once?" The answer isn't bureaucracy. It's risk management.

The Fraud Pattern SBI Prevents:

In the early 2010s, several education loan fraud cases involved students inflating living expense claims, receiving lump-sum disbursements, and using funds for purposes unrelated to education. Some dropped out mid-course but had already received multi-year funding. Banks couldn't recover these amounts because the money wasn't traceable to educational institutions.

SBI's current disbursement structure, tuition paid directly to universities, living expenses released in tranches against verified documents exists to prevent this. When you submit a vague "₹8 lakh for living expenses," RACPC sees it as potential misuse risk, not administrative detail.

Why Documentation Granularity Matters to the Bank:

Every rupee disbursed must be defensible in a loan audit. If a student defaults and the case goes to recovery, SBI must prove the funds went toward legitimate educational expenses. A signed rent agreement proves housing cost. A GIC confirmation proves Canadian visa compliance. A laptop purchase quote proves educational equipment.

Without this documentation trail, SBI cannot legally justify the disbursement even if your sanction was approved.

The Volume vs Accuracy Trade-Off:

SBI disburses over ₹10,000 crore annually in education loans. RACPC handles thousands of files during the May-August peak season. The choice is: process everything fast with minimal verification (high fraud risk) or verify thoroughly (slower but defensible).

They chose the second. This is why students who submit clean, complete documentation move faster than those who submit partial requests expecting "the bank to figure it out." The bank won't. The system is designed to reject incomplete requests, not accommodate them.

Understanding this doesn't make the process easier, but it explains why preparing documentation thoroughly before your first request is not optional, it's the only way the system is designed to work.

The typical SBI education loan disbursement time after sanction is 5 to 10 working days but only if:

What Slows It Down:

The YONO Paradox: Most students assume the YONO app speeds up disbursement because it's digital. In practice, YONO submissions during peak season (May-August) often experience 2-5 day technical delays that branch submissions don't. Why? YONO processes requests through the same RACPC queue but adds a digital verification layer. If your upload fails or document format isn't recognized, you're not notified immediately, you discover it 3-4 days later when checking status. For time-sensitive international transfers or complex GIC/blocked account disbursements, in-person branch submission with immediate document verification often moves faster than the convenient digital option. Convenience and speed are not the same thing.

Your sanction letter is valid for 6 months from the date of issuance. If you do not initiate the SBI loan disbursement process within this period, you typically need revalidation.

Revalidation Process:

Why This Matters: If you're waiting for visa approval or deferring your intake, you can't simply let your sanction expire and expect smooth reactivation. Interest rates in 2025–26 have seen periodic adjustments due to RBI monetary policy shifts. A revalidation may lock you into a higher rate than your original sanction if rates increased during your delay.

The Smarter Approach: If you know your intake is deferred, inform SBI immediately. Some students proactively request partial disbursement (like GIC or blocked account funds) within the 6-month window to keep the loan active, even if tuition disbursement happens later.

Based on real student experiences and counselor observations, here's what actually works:

Prepare Complete Documentation Before Requesting Disbursement Don't submit your disbursement request until you have:

Maintain a 15–20 Day Buffer Between Disbursement Request and Fee Deadline The SBI loan disbursement time after sanction is officially 5–10 days, but unexpected delays happen. If your university fee deadline is June 15, submit your disbursement request by May 25–30. This buffer protects you from last-minute stress if RACPC flags your documents for corrections.

Use YONO Only If Your Documentation Is Already Perfect The YONO app is convenient, but technical glitches during peak traffic periods can delay submissions. If your disbursement request is time-sensitive or involves complex international transfers, visit your branch in person and submit the request manually.

This article references data and policies from the following verified sources:

Primary Data:

Regulatory & Tax:

Visa Compliance:

SBI product terms (interest rates, fees, timelines) reflect publicly available information as of May 2026 and are subject to change. Verify current details with State Bank of India before making financial decisions.

The SBI education loan disbursement process doesn't fail because banks are slow. It fails because students treat disbursement like sanction, a passive milestone where the bank does the work.

Disbursement is active. It requires you to:

The students who move fastest through the SBI loan disbursement process aren't the ones with the highest sanctions or the best universities. They're the ones who understand that documentation clarity is not a formality, it's the entire system.

If you're navigating this process and need guidance on what documents to prepare, how to structure disbursement requests, or when to escalate delays, GyanDhan's education loan counselors provide free support throughout the journey. From eligibility checks to disbursement troubleshooting to repayment strategy, we help students avoid the mistakes that cost time and seats.

SBI education loans cover tuition fees, accommodation (on-campus or off-campus rent), travel expenses to and from the study destination, study materials, gadgets (laptop/tablet if educationally necessary), health insurance, and other education-related costs. Living expenses require detailed breakdowns before disbursement.

The sanction letter confirms SBI has approved your education loan with specified terms — loan amount, interest rate, repayment tenure, and moratorium period. However, no money is released at this stage. The disbursement letter is issued after you submit verified expense documents and confirms the exact amount being transferred under the SBI education loan disbursement process

Yes, but only in specific situations. SBI can pause or reverse disbursement if submitted documents are found incorrect, admission is cancelled or deemed invalid, or visa is rejected (in some cases). Once funds are transferred to the university, reversal depends on the institution's refund policy, which is why accuracy during the education loan disbursement SBI stage is critical.

If your intake is deferred, SBI may hold further disbursements. Already disbursed tuition may be adjusted to the next intake based on university policy. In some cases, partial refunds are routed back to SBI. You must immediately inform the bank to avoid complications in the SBI loan disbursement process and ensure your sanction remains valid.

Under Section 80E of the Income Tax Act, you can claim 100% deduction on interest paid on your education loan with no upper limit on the deduction amount. This benefit is available for 8 years from the start of repayment, making long-term repayment under the SBI education loan disbursement process more financially manageable.

Margin money is the portion of total education cost that the borrower must pay from their own funds. For SBI overseas education loans, this is typically 10%. For example, if your total cost is ₹20 lakh, SBI funds ₹18 lakh, and you contribute ₹2 lakh. This is a key factor during both sanction and SBI loan disbursement time after sanction, as you must specify which expenses are margin-funded versus loan-funded.

Yes. SBI allows pre-visa disbursement for countries like Canada, Germany, Australia, and New Zealand where fee payment or proof of funds is mandatory before visa approval. Tuition fees or GIC/blocked account amounts are directly transferred as part of the SBI education loan disbursement process before you receive your visa.

Yes. You can track disbursement status via the SBI YONO app, net banking portal, or by following up directly with your branch using your RACPC reference number. Tracking helps you stay updated on SBI education loan disbursement time and avoid last-minute delays.

The SBI loan disbursement time after sanction usually ranges from 5 to 10 working days, provided all documents are submitted correctly, the disbursement request form is error-free, the university fee demand is clear, and co-applicant documents are valid. Delays typically occur due to incomplete paperwork or peak admission seasons when RACPC processes high application volumes.

Check Your Education Loan Eligibility

Ask from a community of 10K+ peers, alumni and experts

Trending Blogs

Similar Blogs

Network with a community of curious students, just like you

Join our community to make connections, find answers and future roommates..Country-Wise Loans

Best Lenders for Education Loan

ICICI Bank

Axis Bank

Union Bank

Prodigy

Auxilo

Credila

IDFC

InCred

MPower

Avanse

SBI

BOB

Poonawalla

Saraswat