Help our experts understand you better by filling our 2-Minute Form, to find the right education loan

Get instant loan offer suitable to your profile !

Explore eligibility, process and get a free profile evaluation.

All you need to know about education loans for studying abroad

Study Abroad Expert

An education loan is a financial aid that helps students afford their higher education either in India or abroad. For abroad, different banks offer different loan types based on country and course. You can use the interest rates and the terms to choose the right education loan to study abroad.

However, suppose you have secured admission to a recognized university abroad that ranks among the top 500 QS World Ranking. This can help you get better interest rates and opportunities to cover your tuition and living expenses abroad.

Yet, when you start applying to different lenders it can be overwhelming because of overflowing documentation and formalities. You contact GyanDhan to guide you through this process. We help students find the best education loan for their study abroad needs, tailored to their unique profiles, ensuring a seamless and hassle-free loan approval process.

When you are considering an education loan for abroad studies, students often miss out on some details. Below are the steps that you can follow to build a roadmap to get an education loan:

You can use the Vidya Lakshmi Education Portal to fill out your application. However, you can also use it to explore available scholarships

The first step in getting a loan for study abroad is to calculate the expenses you want to cover. However, each lender has its own list of covered expenses. You can refer to the list below, but ensure to check with the lender. This will help you evaluate your options while applying for the education loan.

Education loan to study abroad are of two types, one that is taken with collateral that is a secured loan, and one taken without collateral that is an unsecured loan. You need to understand the difference between the two before choosing the one that is right for you.

When you get a secured loan from the lender you offer collateral like immovable property, FD, Insurance Policy, etc. against which the loan is offered.

Any property movable or immovable pledged against the collateral as a security against the loan is called collateral. Want to know about the type and documents considered as collateral? Read here.

The amount you can borrow against the collateral may vary based on the lender; however, around 70% to 80% of the collateral value is provided as the loan amount.

When the loan amount is above INR 4 Lakhs, then the bank asks for a guarantor. Being a guarantor is a big responsibility because if an applicant defaults on the loan, he or she will be obliged to repay the education loan.

When the borrower does not have any collateral to get their loan, they usually opt for an unsecured education loan.

When considering student loans for studying abroad, you have three main categories of lenders to choose from:

The lending choices within each category are as follows:

Traditional financial institutions offer education loan to study abroad. The lenders topping the list are:

SBI is everyone's first choice among public banks for a loan to study abroad. They offer an abroad education loan under the Global Ed-Vantage scheme. The key features of the scheme are:

Some people consider PNB for education loans. They offer abroad education loans under the Udaan scheme. The key features of the education loan are:

People often consider private banks when they are looking for an unsecured education loan. The popular leaders in the list are:

ICICI Bank offers education loans to almost every university. However, students with offer letters from top universities can get approval for higher loan amounts. The key features of their education loan are:

Note: ICICI Bank has two categories: Premium and General. The Premium category includes the top 100 universities, while the General category covers almost all universities. Loan amount and interest rate may vary depending on the category.

Axis Bank has a wide range of available universities with a variety of benefits. The key features of their education loan to study abroad are:

Note: Axis Bank has two categories: Prime A and Prime B, which influence the interest rate and loan amount. You can borrow a minimum of INR 40 Lakhs under the Prime A category and INR 25 Lakhs under the Prime B category.

Non-Banking Financial Companies are financial institutions that offer various financial services similar to traditional banks but operate without a banking license.

Credilla is a subsidiary of HDFC Bank and offers competitive interest rates compared to other private banks. The key features of their education loan are:

Note: HDFC Credilla has three categories: A, B, and C, which depend on academic scores. The most preferred exam they evaluate to categorize students is the GRE Exam, but it is not mandatory.

Avanse provides customized education loans for students, covering various expenses in the loan amount. The key features of their education loan are:

Note: Avanse has three categories: A, B, and C, which affect your loan amount based on university and academic scores. You can borrow a minimum of INR 30 Lakhs in category C.

Financial entities based outside your home country that specialize in offering international education loan to study abroad.

MPower can be useful if you don’t have a co-applicant or collateral for the education loan. International lenders are often the last option because they tend to be expensive for students. The key features of their education loan are:

MPOWER Financing has a Path2Success program which provides a comprehensive solution for students planning to study in the USA or Canada. You can leverage some benefits such as visa services, including free preparation courses and mock interviews, financial services like US bank account prequalification and credit cards, and career services. Know more about the Path2Sucees Program.

Prodigy provides education loans for students who want to study abroad. Their network includes over 1,500 schools worldwide. The key features of their education loan are:

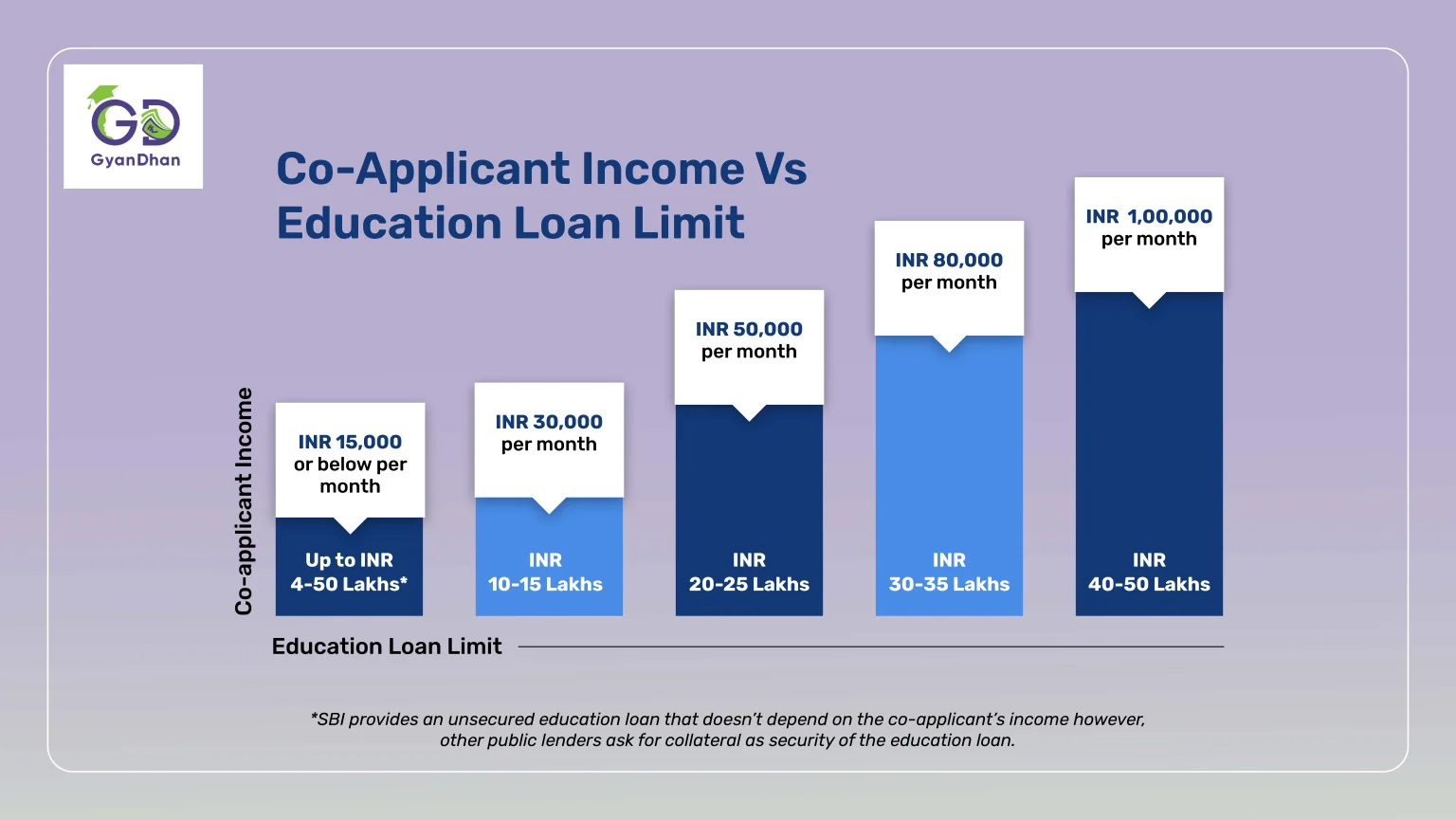

The education loan interest rate varies depending on the student's profile. Your course, university, and country play an important in your education loan amount. However, another factor that affects your interest rate is the co-applicant profile specifically in the unsecured loan options. You can use the table below to refer to the interest rates of the popular lenders.

Education loan abroad eligibility is straightforward but it can vary for different lenders. The general eligibility criteria to get a student education loan for study abroad are listed below -

Education loan required documents vary from lender to lender and also depend on the type of education loan applied for. Here’re the general documents required by almost every lender:

| Document Type | Required Document |

|---|---|

| KYC Documents |

|

| Address Proof |

|

| Academic Record Documents (From Applicant) | |

| Financial Documents from the Co-applicant |

|

| Technical Documents for Collateral (For Secured Loan) |

|

| Legal Documents for Collateral (For Secured Loan) |

|

When you are getting an education loan, you should be aware of the key features that will help you choose the right lender based on your profile.

A comprehensive comparison of some of the best lenders offering education loans is tabulated below in order to find the best education loan for abroad studies. Detailed information on each lender’s loan amounts, interest rates, moratorium periods, and other essential factors is provided, enabling you to make informed decisions.

| Basis of Difference | UBI | SBI |

|---|---|---|

| Loan Amount (Unsecured) | Up to INR 40 Lakh | Up to INR 50 Lakh |

| Interest Rate | Starting at 9.8%* |

10.15% (Men)* 09.65% (Women)* |

| Moratorium Period | Course + 12 months | Course + 6 months |

| Unsecured Loan Eligibility | Only for master program | Top 100 universities |

| Financial Co-applicant Required* | Yes | Yes |

| Processing Fees | 10,000 INR + GST | 10,000 INR + GST |

| Processing Time | Up to 15-20 days | Up to 14 days |

| Margin Money | 10-15% | 10-15% |

| Repayment Tenure | 15 years | 15 years |

| Repayment Options* | Full Moratorium and PSI | Full Moratorium and PSI |

| Premiere Institute List | Have a list that can lead to fluctuation in interest rate | Have a list that includes the top 100 universities |

| Loan Approval Basis GRE / GMAT? | No | No |

| Tax Benefit* | Yes | Yes |

SI - Simple Interest; PSI - Partial Simple Interest; EMI - Equated Monthly Installment

*Interest rate as of January 2026

| Basis of Difference | IDFC First Bank | ICICI Bank | Axis Bank |

|---|---|---|---|

| Maximum Loan Amount | Secured loans - INR 1 cr, Unsecured loans - INR 75 Lakh | Secured loans - INR 1 cr, Unsecured loans - INR 40 Lakh | Up to INR 40 - 75 Lakh |

| Interest Rate | 11.50 - 12.25% | 9.85 - 15.5% | 11 - 11.5% |

| Moratorium Period | Course period + 12 months | Course period + 6 months | Course period + 12 months |

| Unsecured Loan Eligibility | Only for master program | Only for approved courses | Only for approved courses |

| Financial Co-applicant Required* | Yes | Yes | Yes |

| Co-applicant Minimum Income | INR 35,000 / per month | INR 60,000 / per month | INR 35,000 / month |

| Processing Fees | 1 - 1.25% | 0.5 - 2% | 0.75% of the loan amount + GST |

| Processing Time | Up to 15-20 days | Up to 14 days | - |

| Margin Money | Nil | 0 - 15% | 0 - 5% |

| Repayment Tenure | 12 years | 8 - 12 years | 15 years |

| Repayment Options* | Simple or Partial Interest | Simple Interest (SI) | Simple Interest (SI) |

| Pre-approved College Lists | Colleges and universities are divided into three categories i.e. Platinum, Titanium, and Gold | Colleges and universities are divided into four categories i.e A1, A2, A3 & A4 | Colleges and universities are divided into four categories A, B, C, and D |

| Loan Approval Basis GRE / GMAT? | Yes | No | Yes |

| Tax Benefit* | Yes | Yes | Yes |

*Interest rate as of January 2026

| Features | HDFC Credila | Avanse | Auxilo | InCred |

|---|---|---|---|---|

| Maximum loan amount | INR 20 - 75 Lakh | INR 20 - 75 Lakh | INR 20 - 75 Lakh | INR 20 - 80 Lakh |

| Interest rate* | 11.25 - 13% | 12.25 - 14% | 12 - 13.25% | 11.65 - 13.5% |

| Moratorium period | Course period + 1 year | Course period + 1 year | Course period + 1 year | Course period + 1 year |

| Unsecured loan eligibility | Only for master program | Only for master program | Only for master program | Only for master program |

| Financial co-applicant required* | Yes | Yes | Yes | Yes |

| Minimum co-applicant income (negotiable for secured education loans) | INR 30,000 - 60,000 | INR 30,000 - 60,000 | INR 20,000 - 40,000 | INR 20,000 - 40,000 |

| Processing fee | 0.5 - 1.5% of the loan amount + GST | 1 - 2% of the loan amount + GST | 0.5 - 1.5% of the loan amount + GST | 0.5 - 1% of the loan amount + GST |

| Processing time | Up to 7-10 days | Up to 14 days | Up to 5-7 days | Up to 10 days |

| Margin Money | Nil | Nil | Nil | Nil |

| Repayment tenure | 12 - 15 years | 12 - 15 years | 12 - 15 years | 12 - 15 years |

| Repayment Options During Moratorium* | Simple Interest (SI) or partial Simple Interest (PSI) | Simple Interest (SI) or partial Simple Interest (PSI) | Simple Interest (SI) or partial Simple Interest (PSI) | Simple Interest (SI) or partial Simple Interest (PSI) |

| Tax benefit* | Yes | No | No | No |

*Interest rate as of January 2026

If you are getting an education loan to study abroad, you can take advantage of the following features:

Applying for student loans India studies abroad can be quite simple if done carefully. To help you answer the question, 'How do I get an education loan for abroad studies?' here are some steps that will assist you.

Refer & Earn Unlimited!

Earn ₹3,000 for every successful referral. Plus, get a ₹10,000 bonus every time you hit 5 referrals.

No limits! Keep referring. Keep earning.

Multiple lenders to choose from

Tailored solutions that save money and time to support your academic journey

Our free tools will help you out.

A smart algorithm that guides every step of your education journey.

See your loan options upfront: quick, free, and accurate.

Check Eligibility

Determine your EMIs and repayment schedules before committing to a student loan.

Calculate Now

Project your potential future earnings and compare countries based on return on investment.

Estimate Now

Get insights on income, employability, costs, and top recruiters of upto 4 universities.

Compare Now

Get your Statement of Purpose evaluated on matter, grammar, readability using Natural language processing.

Submit SOP

Convert your percentage or 10-point CGPA to GPA score with just a single click.

Convert Now