Help our experts understand you better by filling our 2-Minute Form, to find the right education loan

Get instant loan offer suitable to your profile !

On this Page:

Explore public sector bank education loans for higher studies in India and abroad. Get details on loan eligibility, benefits, interest rates, and more.

Financing higher education with an education loan is daunting. Not only do you have to search for a product that covers your expenses, but you also have to search for one that doesn’t blow a hole through your pocket. After all, an education loan is a financial responsibility for at least a decade and you should select a product that will help you finance your education while saving your money.

We, at GyanDhan, will make this whole process easy for you. Below is a detailed comparison of education loans offered by various public sector banks. Refer to this before you settle on a lender.

Let’s get into it -

Every public sector bank in India offers an education loan to study in India. However, not every bank has a loan product for education abroad. Some of the top banks that offer education loans to study in India and abroad are as follows -

| Particulars | Details |

|---|---|

|

Loan Amount |

Up to INR 1.5 crore for abroad studies |

|

Interest Rate |

9.65% (Men), and 10.15% (Women) for abroad studies |

|

Processing Fee |

INR 10,000 + taxes on loans above INR 20 lakhs |

|

Loan Tenure |

15 years |

|

Moratorium Period |

Course duration + 6 months |

|

Margin Money |

10% of the loan amount |

| Particulars | Details |

|---|---|

|

Loan Amount |

For abroad – Up to INR 1.5 cr |

|

Interest Rate |

For abroad – 9.7% - 10.50% |

|

Processing Fees |

INR 10,000 + GST |

|

Loan Tenure |

15 years |

|

Moratorium Period |

Course period + 6 months |

|

Margin Money |

10% above INR 4 lakhs |

| Particulars | Details |

|---|---|

|

Loan Amount |

Upto INR 40 lakhs |

|

Interest Rate |

7% - 10% |

|

Processing Fees |

NIL |

|

Loan Tenure |

15 years |

|

Moratorium Period |

Course duration |

|

Margin Money |

Above INR 4 lakhs 5%-15% to study abroad |

| Particulars | Details |

|---|---|

|

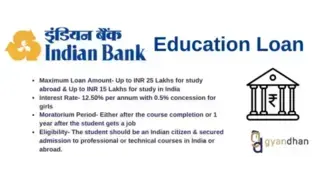

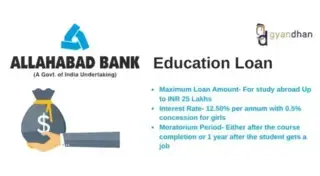

Loan Amount |

INR 150 lakhs for abroad studies |

|

Interest Rate |

Up to 7.5 lakhs - 1 Year MCLR +1.70% Above 7.5 lakhs - 1 Year MCLR + 2.50% |

|

Processing Fees |

For abroad – INR 5000 |

|

Loan Tenure |

15 years |

|

Moratorium Period |

Course Duration |

|

Margin Money |

5% - 15% |

| Particulars | Details |

|---|---|

|

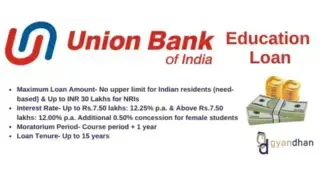

Quantum of Finance |

20 lakh for studies abroad |

|

Interest Rate |

8.10- 10.6% |

|

Processing Fees |

Loans up to INR 10 lakhs – INR 500 Loan above INR 10 lakhs – INR 1000 |

|

Loan Tenure |

15 years |

|

Moratorium Period |

Course Period + One Year |

|

Margin Money |

Upto Rs. 4 lacs: NIL In India Above Rs. 4 lacs: 5% In Abroad Above Rs. 4 lacs:15% Margin |

| Particulars | Details |

|---|---|

|

Quantum of Finance |

For abroad – INR 150 lakhs |

|

Interest Rate |

12.05% to 14.55% |

|

Processing Fees |

NIL |

|

Loan Tenure |

15 years |

|

Moratorium Period |

Course duration |

|

Margin Money |

NIL up to 4 lakhs 5% upto 7.50 lakhs 15% above 7.50 lakhs |

| Particulars | Details |

|---|---|

|

Quantum of Finance |

For abroad studies – INR 40 lakhs |

|

Interest Rate |

Institute under list A - RLLR-0.60%=8.75% Institute under list B - RLLR-0.35%=9.00% |

|

Processing Fees |

NIL |

|

Loan Tenure |

10- 15 years |

|

Moratorium Period |

Course duration |

|

Margin Money |

5-15% |

| Particulars | Details |

|---|---|

|

Loan Amount |

PNB Udaan - up to 2 crores PNB Pratibha - up to 35 lakhs |

|

Interest Rate |

PNB Udaan - 9.25% for the top 50 listed universities PNB Pratibha - 8.10-% - 9% PNB Saraswati - 10.50% for males and 10.00% for females |

|

Processing Fees |

For abroad studies- 1% Minimum Rs.10000/- (Refundable after 1st Disbursement) |

|

Loan Tenure |

15 years |

|

Moratorium Period |

Course duration |

|

Margin Money |

Up to 4 lakhs - NIL Up to 7.50 lakhs - 5% Above 7.50lakhs - 15% |

| Particulars | Details |

|---|---|

|

Loan Amount |

Need-based financing |

|

Interest Rate |

9.45% |

|

Processing Fees |

0.50% of the loan amount is charged for abroad studies (refundable if the borrower does not pursue the course). |

|

Loan Tenure |

15 years |

|

Moratorium Period |

Course Duration |

|

Margin Money |

NIL up to 4 lakhs Above 4 lakhs for study abroad - 15% |

| Particulars | Details |

|---|---|

|

Loan Amount |

Need-based finance |

|

Interest Rate |

8.80% to 11.40% |

|

Processing Fees |

Upto ₹10 lakhs - Nil Above ₹10 lakhs - 0.15% (maximum INR 3000) |

|

Loan Tenure |

10- 15 years |

|

Moratorium Period |

Course Duration |

|

Margin Money |

5% -15% |

We will be comparing the education loan products of some of the top public banks from the above-mentioned list to find the best bank with the best loan product.

Choosing the right education loan, from the right lender can be overwhelming since the education loan provided by each lender comes with various pros and cons. However, choosing a public sector bank for an education loan can be highly advantageous for you. Public sector banks offer student-friendly loan terms which are designed to support student's higher education. Below are the b

Check Your Education Loan Eligibility

Ask from a community of 10K+ peers, alumni and experts

Trending Blogs

Similar Blogs

Network with a community of curious students, just like you

Join our community to make connections, find answers and future roommates..Country-Wise Loans

Best Lenders for Education Loan

ICICI Bank

Axis Bank

Union Bank

Prodigy

Auxilo

Credila

IDFC

InCred

MPower

Avanse

SBI

BOB

Poonawalla

Saraswat