Help our experts understand you better by filling our 2-Minute Form, to find the right education loan

Get instant loan offer suitable to your profile !

On this Page:

Learn how a student repaid a ₹45 lakh education loan in just 3.5 years using smart EMIs, lump-sum prepayments, and disciplined budgeting.

Education loans have made international education dreams more affordable today. An education loan of ₹45 lakh is seen as an expensive dream at first, but for one of our customers, a student who went to the US for a Master’s in Finance, it turned out to be a manageable and well-planned journey.

Like most students, Anjali went for a 15-year loan tenure, assuming she would repay it gradually over time. But after completing her Master’s degree in the US and securing a job, she did something different. Instead of letting the loan run its full course, she planned her repayments smartly and paid off the entire ₹45 lakh education loan within just 3.5 years of starting her career.

What made this possible was not an unrealistically high salary but a clever repayment strategy, disciplined budgeting, and smart use of loan features.

In this blog, we break down Anjali’s education loan journey, explain how she repaid her loan within 3.5 years of tenure, and can help many other students in repaying their education loans. This information doesn’t apply to the U.S., but it can be used by students studying in the UK, Germany, Ireland, and Australia to repay their education loans faster and save lakhs in interest.

Before we discuss Anjali’s repayment strategy, it’s important to understand a few common education loan terminologies. These features would help you plan your repayment strategy for your education loan.

Loan tenure refers to the total time given by the lender to repay the education loan. In India, education loans usually have a tenure of up to 10–15 years.

Most students, including Anjali, at first opt for a 15-year tenure. However, it’s important to note that choosing a longer tenure does not mean you must use it fully. It simply gives flexibility to repay faster when your income allows. That’s why we often advise students to go with a longer tenure to avoid unforeseen circumstances.

The moratorium period is the time during which the student is not required to pay EMIs. It usually includes:

During this period:

Students can choose between:

Anjali opted for a full moratorium, as she wanted to avoid the repayment burden, and this option helped her afford her monthly expenses.

A co-applicant is mandatory for most education loans in India. For an unsecured education loan, it is mandatory, and it also affects the loan terms. Most banks generally approve the following people as co-applicants:

The co-applicant:

While the student is studying, the financial liability rests on the co-applicant. Anjali was mindful of this responsibility; therefore, opted for the full moratorium to reduce pressure on her family.

One of the biggest advantages of education loans is that most lenders don’t charge prepayment or foreclosure penalties. This feature helps borrowers make lump-sum payments anytime and save significantly on interest.

This feature played a key role in Anjali’s accelerated repayment journey. Still, ask your loan counselor about the prepayment penalty.

Once Anjali completed her Master’s in Finance in the US and secured her first full-time job, she did not immediately start aggressive loan repayment, even though she could afford to. Instead, she took a calculated approach for the first year after getting a job. Anjali focused on:

She parked her savings across low-risk and moderately liquid instruments such as high-interest savings accounts, short-term deposits, and conservative debt instruments so the money could earn returns while remaining accessible.

When her EMI began after the moratorium, she started paying installments, which allowed her savings accumulate interest. At the end of the first repayment year, Anjali used half of her savings to repay a large chunk of the loan amount.

This strategy was based on three loan features:

Each of these played a distinct role, but we are not revealing the whole maths because it needs some clarification first.

Anjali opted for a full moratorium period during her two years of Master's program, including an additional 12 months as a moratorium period. This feature actually helped her gain some time without any repayment pressure.

But, it affected her principal amount because her loan grew from ₹45 lakh to approximately ₹52–53 lakh. However, she was aware of it and included this in her repayment strategy.

During the moratorium period, Anjali did not make any EMI payments. As a result, when the moratorium ended, the loan accumulated interest, which affected her EMI. At this stage, the standard repayment structure felt high.

But, instead of accepting this default structure, Anjali approached her lender and requested a salary-linked EMI and repayment structure, commonly known as the EMI bump-up strategy.

The EMI bump-up strategy helped her start with a lower or manageable EMI and gradually increase the EMI with their salary growth. This option is helpful for students who began their careers with moderate salaries.

By choosing a salary-linked EMI bump-up converted her heavy repayment burden into a structured and predictable repayment plan.

One of the most underutilized benefits of education loans in India is penalty-free prepayment. But Anjali made full use of this feature by using her annual bonuses, performance incentives, savings, and Section 80E returns to make a full prepayment of the education loan in 3.5 years.

Instead of putting all the money into EMI, Anjali strategically used her:

Each prepayment adjusted the principal amount, which had an immediate and long-term impact. Reducing the principal early lowered the interest calculated in subsequent months, ensuring that a higher portion of EMI went toward closing the loan rather than servicing interest.

Another advantage of lump-sum prepayment is its flexibility. Whenever she accumulated a meaningful surplus through bonuses or tax refunds, she made a prepayment.

By combining lump-sum prepayments with increasing EMIs, Anjali significantly compressed the loan tenure, helping her save several lakhs in interest that would otherwise have been paid over a much longer period.

This strategy highlights an important lesson for borrowers: it’s not just how much you earn, but how strategically you prepay, that determines how fast an education loan can be closed.

After coming to this blog, you became curious to find out, “How to pay off a 45 lakh education loan fast?” The answer lies in her repayment strategy and budget, which we have discussed below.

Living in the United States is expensive, with all those rent, insurance, transport, and everyday expenses. But for Anjali, budgeting discipline became a great headstart which accelerated loan repayment, even without extreme financial pressure.

Therefore, to repay her loan faster, she consciously kept track of her expenses. But, how?

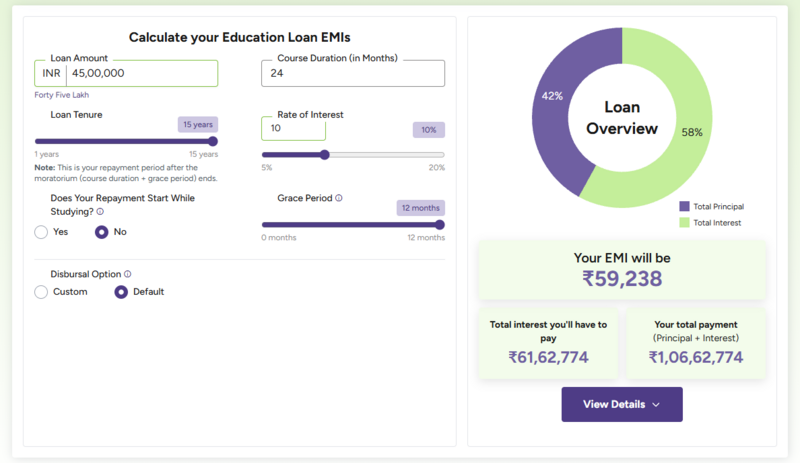

To make this work, she planned a monthly structure, which gave her clarity. At the time, her standard EMI and repayment structure were as shown in the image below.

For a ₹45 lakh education loan at 10% interest, the structure shown above assumes a total tenure of 6 years, including the study period and grace (moratorium). So, the repayment begins after course completion, with the loan designed to close within the overall 6-year window.

The repayment structure for 3.5 years, excluding the moratorium, looked like:

During her 2-year course and grace period, she made no mandatory repayments. Once she graduated and started working, instead of immediately paying a heavy EMI burden, she prioritized budget discipline and income stability.

During her master’s, she worked part-time on campus and took up paid summer internships. Over three years, her total income during study came to around ₹28 lakh. Living in the U.S. is expensive, but she kept costs under control through shared housing, basic living, and no lifestyle splurges.

Even after expenses, family support, and daily costs, she managed to save about ₹8 lakh. She invested in low-risk instruments, earning close to 6% annually. By the time she graduated and started working, this fund had grown to about ₹9.5 lakh. This money became the foundation of her repayment strategy.

After graduation, Anjali secured a finance role in the U.S. with an average entry-level package. Her monthly take-home salary was around ₹4.5 lakh. Even after getting a job her monthly expenses stayed close to ₹1.9 lakh, even after getting a job. She started her loan repayment with a salary-linked EMI of ₹1.2 lakh, not the maximum possible EMI. That still left her with about ₹1.4 lakh every month in savings.

By the end of her first working year, she had paid ₹14.4 lakh in EMIs and saved ₹16.8 lakh from her salary. But, at the end of the year, she earned ₹6 lakh in bonuses and incentives. Therefore, in one year, she built a repayment-ready corpus of over ₹37 lakh.

| Stage | What Happened | Amount (₹) |

|---|---|---|

|

Loan Taken |

Education loan for U.S. Master’s |

45,00,000 |

|

Moratorium |

2 years study + 1 year grace |

No EMI |

|

Savings during study |

Part-time + internships |

8,00,000 |

|

Interest earned on savings |

~6% over 3 years |

1,50,000 |

|

Corpus at job start |

Ready for repayment |

9,50,000 |

|

EMI paid (Year 1 job) |

₹1.2L × 12 months |

14,40,000 |

|

Salary savings (Year 1) |

₹1.4L × 12 months |

16,80,000 |

|

Bonuses & incentives |

2 years |

10,00,000 |

|

Lump-sum prepayments |

Multiple installments |

36,30,000 |

|

Total repayment |

EMI + lump sums |

~₹67 lakh |

|

Total interest paid |

Approximate |

₹22 lakh |

|

Loan closed in |

Including moratorium |

5.5 years |

Anjali's case describes a powerful case on how to pay off a 45 lakh education loan fast. This is not the only way to repay the education loan faster. We have discussed some more prepayment education loan India tips below for your reference:

Many students opted for the full moratorium period, because it looks easy and practical. But paying even ₹2,000–₹5,000 per month during the study period helps in two major ways. First, reduces interest compounding and lowers the post-study EMI pressure. Therefore, students should go for a partial interest payment or a full S.I. payment if they have a steady income source.

Even though you are unable to pay the education loan repayment in 3 years, you can still reduce the loan tenure by paying one extra EMI every year. This extra EMI yearly goes towards the principal amount, which will subsequently reduce the interest in the long term.

Note: These scenarios apply to all education loans; repayment math remains the same across countries. What changes is the speed, based on salary levels and cost of living.

Anjali’s journey became one of the loan repayment success stories in India and has given tips for prepayment of education loans from India to many students. It clearly shows that a high education loan amount does not have to be a limitation.

So, if you are also planning to go abroad for education and are limiting yourself because of funds, this is a powerful real-life example. A student can increase their earning potential after studying abroad and confidently repay the education loan. You just require a clear repayment strategy and financial discipline in place.

If you need personal guidance, check your education loan eligibility today and take the first step toward funding your global education.

Read More:

Yes. With aggressive EMIs, lump-sum prepayments, and disciplined budgeting, it is achievable. Post-study salaries in countries like the U.S., Germany, the UK, and Australia allow borrowers to increase EMIs gradually and make principal-heavy prepayments. A loan originally structured for 15 years can be closed in as little as 3–5 years without financial strain.

Yes. Even small monthly payments during the study period can significantly reduce the total interest rate. Paying ₹2,000–₹5,000 per month during the moratorium helps control interest compounding and prevents interest from getting added to the principal.

In most cases, Indian banks and NBFCs do not charge prepayment penalties on education loans, especially when repayments are made from the borrower’s own income. Few banks impose a prepayment penalty in case the repayment is made within 6-12 months of sanction.

The United States and Germany offer the fastest repayment potential due to favorable salary-to-loan-size ratios.

Check Your Education Loan Eligibility

Ask from a community of 10K+ peers, alumni and experts