.webp)

.webp)

Help our experts understand you better by filling our 2-Minute Form, to find the right education loan

Get instant loan offer suitable to your profile !

On this Page:

Explore guide on education loan disbursement in India, detailing the step-by-step process, types of disbursements, eligibility criteria, & tips to overcome challenges.

“What is disbursed amount in loan?”. The answer to this question, when first heard, will make your head spin. Yet, we won’t let that happen because we have disclosed everything that a bank would not disclose. Everything starts when you start exploring the lenders for your education loan.

Well, the sanctioned letter and the amount written on it are an official declaration that informs the amount of funds the lender is going to provide for the next 2-3 years for your education. However, the sanction and disbursed amount are always different from the disbursement of education loan. Because the amount is disbursed based on the semester fee, thus, the sanction amount is fully consumed in the last year of the university or college. Let’s learn about this concept in more detail.

The disbursed amount of the loan is the amount that the lender transferred to the university as your tuition fee and some additional expenses, such as housing, books, travel, and other costs that a student requires to support their studies abroad.

Therefore, when a student is relying on an education loan, they need to ensure that they will get the resources they need to settle and sustain their living abroad. Therefore, when you receive the sanction letter and get the approval for your visa. Confirm the dates with the lender on the first disbursement.

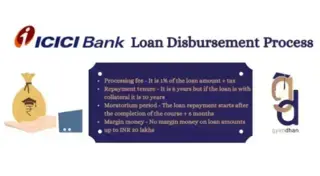

Many banks, such as Prodigy, disburse the amount when you acknowledge the terms and conditions within the new network. Many other lenders, such as ICICI Bank, BOB, and Yes Bank, transfer the first semester tuition fee when you accept and sign the loan agreement. Thus, your loan application form and the Letter of Acceptance decide the whole disbursement process of the loan amount.

Here are the different types of disbursement in education loans -

The full loan amount is disbursed to the student in one installment when this kind of disbursement occurs. With this approach, the student has the freedom to manage and distribute money for living expenses, books, supplies, room & board, and tuition as needed. Usually, a cheque or a direct transfer into the student's bank account is used for direct student disbursement. Although it necessitates cautious financial management, this strategy is advantageous for students who have the self-control to plan their costs throughout their academic careers.

With this kind of disbursement, the loan amount is divided into discrete portions. The student receives the component for living expenses, while the portion for tuition is paid directly to the educational institution. This approach reduces the possibility of student misallocation by guaranteeing that necessary expenses like tuition are paid immediately. It gives students the freedom to budget their daily living expenses while also providing the guarantee that tuition and other fees are paid in full.

When a loan is partially disbursed, it is released in installments or stages, usually in accordance with the academic calendar, for example, at the start of each semester or year. This can be used for both living expenses that are reimbursed to the student and tuition fees that are paid straight to the school. The student will have access to the money they need for their education without having to take home a large lump sum all at once thanks to this phased method, which helps to match the release of funds with the real needs as they arise.

When it comes to school loans from Indian banks, direct student disbursement is feasible if the loan is meant to pay for living expenses, books, travel, and other miscellaneous charges in addition to tuition fees. When a student is studying overseas or when the college does not handle all of the student expenses directly, this approach is frequently utilized. When banks have evaluated the creditworthiness and money management abilities of the student or guarantor, they may decide to pay out directly. Direct distribution may also be taken into consideration for part-time or vocational courses in which tuition is not the main cost.

Co-applicants and guarantors play a major role when you are withdrawing an unsecured education loan. Their financial capacity can influence both the approval and the disbursement of education loan speed.

A co-applicant (either parent, guardian, or sibling), alongside the primary applicant. They share the responsibility of loan repayment and act as a security. A guarantor, on the other hand, agrees to repay the loan if the borrower and co-applicant fail to do so.

For both co-applicants and guarantors, the following are important:

If your financial profile does not meet the lender's criteria, then the co-applicant's profile is being considered for securing an education loan. Their stable income helps the lender to mitigate the risk of default. A strong financial profile of the co-applicant also helps in the quick approval of your loan.

In short, choosing a financially strong co-applicant or guarantor is not just a formality; it's a necessity that directly impacts the ease and success of your education loan journey.

Getting an education loan sanction letter is the primary eligibility requirement for your education loan disbursement. However, there have been rejections even after obtaining a sanction letter mostly due to documentation issues. Make sure you submit the documents correctly for a timely disbursement of your education loan. Here are the general eligibility criteria for education loan disbursement:

An education loan's disbursement is a well-planned procedure intended to guarantee a seamless transfer of cash from the lender to the borrower. Understanding this procedure can help borrowers budget for and manage their education more effectively, resulting in a more predictable and seamless path to reaching their academic goals.

Getting an education loan sanctioned is important, while you are planning for your higher education. The time taken for loan approval can vary based on the lender, the type of loan (secured or unsecured), and on your documents. Generally, public banks may take a little longer as compared to private banks and NBFCs.

| Bank/NBFC Name | Time to Sanction (Approx.) | Last Step Before Disbursement | Disbursement Time (Post Sanction) |

|---|---|---|---|

|

12–15 working days |

Document verification and loan agreement |

3–5 working days |

|

|

5–7 working days |

Loan agreement signing |

2–3 working days |

|

|

7–10 working days |

Submission of collateral and agreement |

3–4 working days |

|

|

5–8 working days |

Final approval and agreement |

2–3 working days |

|

|

3–5 working days |

E-sign of agreement |

1–2 working days |

|

|

4–6 working days |

Final offer acceptance |

2–3 working days |

|

|

5–7 working days |

KYC and agreement sign |

2–4 working days |

The loan sanction and education loan disbursement letter is the first document to be issued upon approval of an education loan. This document, which includes information on the authorized loan amount, terms of disbursement, and the payment schedule, acts as an official confirmation from the lender. It is necessary that the borrower carefully reads this letter, since it establishes the parameters for the subsequent financial transactions and describes how the loan will be disbursed, either directly to the educational institution or into the borrower's account.

A crucial step in the loan disbursement procedure is the payment of the borrower's tuition fees, which guarantees that the educational institution is compensated for their costs. Funds may be disbursed into the borrower's account for additional payment or paid straight to the institution, depending on the terms of the loan arrangement between the borrower and the lender. By guaranteeing that tuition payments are made on time, this direct payment method protects the loan's main objective and ensures the student's enrollment and continuous education.

The living expenditure reimbursement program takes care of the borrower's ongoing financial needs as they pursue their education, particularly for international students. Funds can be transferred directly to the student's account by lenders or made available through prepaid FOREX cards. These grants are meant to help students with living expenditures such as housing, food, transportation, and other living costs, giving them the financial freedom to concentrate on their academics without having to worry about money problems. Ensuring that students can afford their living expenses during their academic program requires careful handling of these monies.

To request an education loan disbursement letter, you must submit the below-mentioned documents. These documents help the bank verify your request and ensure the loan amount is disbursed accurately and on time.

Public banks and NBFCs have different methods for disbursing education loans, and each has its own procedure. A comparison illustrating these variations can be found below.

| Basis of Difference | Public Banks | NBFCs |

|---|---|---|

|

Disbursement letter |

Usually required, detailing disbursement terms and conditions. |

Not always mandatory, often offering more flexibility. |

|

Tuition fee disbursement |

Funds are often sent directly to educational institutions or disbursed via specific instruments like FOREX cards. |

Generally offer direct disbursement to the student's account or the institution, based on preference. |

|

Living expenses |

Funds for living expenses are usually transferred to a FOREX card or the student's account, facilitating overseas spending. |

Direct disbursement to the student's account is common, providing immediate access to funds for living expenses. |

|

Processing time |

Tends to be longer due to extensive documentation and procedural requirements. |

Usually quicker, thanks to streamlined processes and fewer bureaucratic hurdles. |

The payout schedule is a set timetable that specifies how and when the money from the education loan will be disbursed. This timetable is essential for financial planning since it tells the borrower when funds will be available for living expenses and tuition. The academic calendar, the lender's processing delays, and certain payment deadlines established by educational institutions are some of the factors that affect the schedule. Borrowers can avoid any disruptions in their education caused by financial inadequacies by making sure their financial needs and academic requirements are in line by having a clear understanding of the payment plan.

There are many obstacles to overcome when navigating the education loan disbursement process, which could prevent the money from transferring smoothly. In order to overcome these obstacles and make sure that financial concerns do not interfere with academic endeavors, awareness and preparedness are essential.

Also Read:

Check Your Education Loan Eligibility

Ask from a community of 10K+ peers, alumni and experts

Trending Blogs

Similar Blogs

Network with a community of curious students, just like you

Join our community to make connections, find answers and future roommates..Country-Wise Loans

Best Lenders for Education Loan

ICICI Bank

Axis Bank

Union Bank

Prodigy

Auxilo

Credila

IDFC

InCred

MPower

Avanse

SBI

BOB

Poonawalla

Saraswat